Land

How to assess land purchase for development

TESA · July 12, 2026 · 9 min read

How to assess land purchase for development

A land purchase assessment is a structured evaluation of zoning, environmental constraints, financial feasibility, and market conditions that determines whether a parcel can be profitably developed before any capital is committed. Developers who skip this process routinely discover deal-killing problems after closing, when remedies are expensive and options are limited. The industry term for this process is development due diligence, and it covers everything from title review to pro forma modelling. Frameworks from bodies like the Urban Land Institute and the National Association of Home Builders treat this evaluation as non-negotiable. The land acquisition process typically runs 30–90 days from identification to closing.

How to assess land purchase for development: setting your criteria first

The most common error developers make is reactive deal evaluation. They wait for a listing to appear, then scramble to assess it without a clear framework. A defined acquisition “buy box” solves this problem before it starts.

A buy box is a written set of acquisition criteria that filters opportunities before any detailed analysis begins. It should specify parcel size range, compatible zoning designations, target geographies, maximum purchase price, and minimum yield thresholds. Developers who define these parameters proactively spend less time on deals that will never work.

Once the buy box exists, targeted site identification becomes faster and more reliable. GIS mapping platforms, municipal parcel databases, and aerial imagery let developers screen sites digitally before visiting them in person. Environmental overlay layers reveal flood plains, conservation authority boundaries, and contamination risk zones at a glance.

The core data sources for initial screening include:

- Zoning code databases (municipal official plans and zoning bylaws)

- GIS and aerial imagery for topography, access points, and land coverage

- Environmental overlays for flood zones, wetlands, and brownfield designations

- Title registry records for ownership history and registered encumbrances

- Utility infrastructure maps for water, sewer, gas, and hydro proximity

Pro Tip: Run a digital triangulation of zoning, environmental overlays, and aerial imagery before making any site visit. This step alone eliminates the majority of unsuitable parcels without spending a dollar on professional fees.

What does comprehensive due diligence on development land involve?

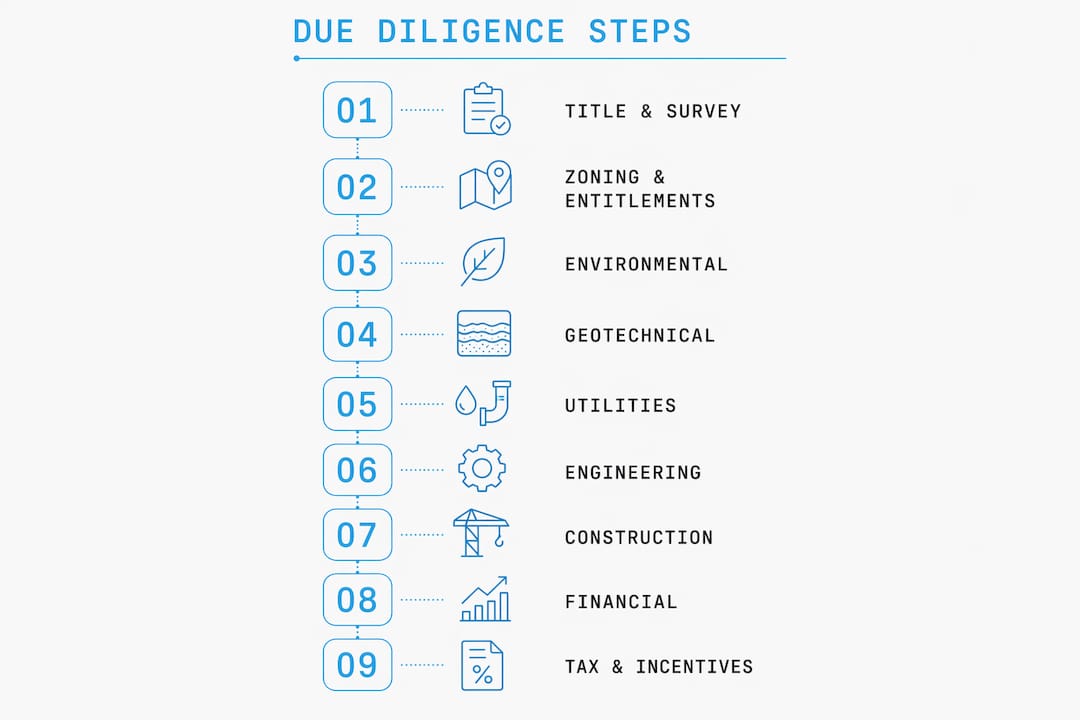

Comprehensive due diligence for development land covers nine standard categories. Missing even one of them is a leading cause of post-closing failures.

The nine due diligence categories

Title and survey confirms legal ownership, identifies easements, rights-of-way, and encumbrances that restrict development. A registered easement running through the centre of a parcel can eliminate an entire building envelope.

Zoning and entitlements establishes what the land is permitted to accommodate: density limits, setbacks, height restrictions, and permitted uses. Rezoning is possible but adds cost and timeline risk that must be priced into the deal.

Environmental covers Phase I and Phase II Environmental Site Assessments (ESAs). A Phase I reviews historical land use for contamination risk. A Phase II involves physical sampling when Phase I flags concerns. Contaminated sites can cost more to remediate than the land is worth.

Geotechnical and soils tests bearing capacity, groundwater depth, and soil composition. Poor soils drive up foundation costs significantly and can make certain building types unviable.

Utilities and infrastructure maps the distance and capacity of water, sanitary sewer, storm sewer, gas, hydro, and telecommunications. Extending services to a remote parcel can add hundreds of thousands of dollars to a project budget.

Engineering and architecture produces concept plans and preliminary cost estimates to test whether the intended development fits the physical site.

Construction and permits reviews local building permit processes, development charges, and any site-specific approval requirements.

Financial and pro forma models all revenues, costs, and returns to determine whether the project meets the investor’s yield target.

Tax and incentives identifies applicable development charges, property tax classifications, and any available government incentive programs.

| Due diligence category | Key focus | Typical timing |

|---|---|---|

| Title and survey | Encumbrances, ownership, boundaries | Early stage |

| Zoning and entitlements | Permitted uses, density, rezoning risk | Early stage |

| Environmental (Phase I/II) | Contamination history and testing | Mid stage |

| Geotechnical and soils | Bearing capacity, groundwater | Mid stage |

| Utilities and infrastructure | Service availability and cost | Mid stage |

| Financial and pro forma | Revenue, costs, returns | Ongoing |

Pro Tip: Sequence your due diligence to check deal-killers first. Confirm zoning compatibility and run a Phase I ESA before commissioning geotechnical reports or architectural concepts. This staged approach protects your budget from early over-commitment.

Early technical screening using GIS mapping and aerial imagery catches deal-killers like steep slopes or utility gaps before costly professional studies begin. Broker-provided maps frequently miss site-level constraints that independent data sources reveal.

How do you calculate financial feasibility for a land development project?

Residual land value is the most direct method for determining the maximum price a developer can pay for a parcel without sacrificing profit targets. The formula is straightforward: completed property value minus total development costs minus the developer’s target profit margin equals the residual land value.

This number tells you what the land is worth to you, not what the seller is asking. If the residual land value is below the asking price, the deal does not work at your required return. No amount of optimism changes that arithmetic.

Key financial metrics in land assessment

| Metric | Role in decision-making |

|---|---|

| Residual land value | Sets the maximum defensible offer price |

| Development yield | Measures net income as a percentage of total cost |

| Spread | Gap between yield and prevailing cap rate; indicates profit margin |

| Net present value (NPV) | Discounts future cash flows to today’s dollars |

| Stabilized NOI | Projected income once the project reaches full occupancy |

| Exit cap rate | Assumed cap rate at sale; drives terminal value assumptions |

The pro forma is the financial model that ties all these metrics together. It projects revenues by unit type, models construction costs, financing costs, carrying costs, and development charges, then calculates the return on invested capital. A development feasibility study tests whether the project pencils before any irreversible commitments are made.

Sensitivity analysis is the discipline that separates experienced developers from optimistic ones. Running the pro forma under multiple scenarios, including a 10% cost overrun, a six-month construction delay, and a softening in exit cap rates, reveals how much margin the deal actually carries. A project that only works under best-case assumptions is not a viable project.

Pro Tip: When comparable sales data is thin, apply a risk discount to your revenue assumptions rather than using the highest available comp. Overestimating revenues is the single most common cause of failed development pro formas.

What market conditions should you analyse before acquiring development land?

Market analysis validates whether demand exists for what you plan to build. Financial modelling is only as reliable as the revenue assumptions it rests on, and those assumptions must come from real market data.

Comparable sales analysis is the foundation. Comparable land sales must match not just parcel size but also accessibility, utility availability, and terrain. A sale that looks similar on paper but sits on serviced flat land is not a valid comp for an unserviced hillside parcel.

For subdivision projects, the analysis requires an additional layer of detail:

- Absorption rate measures how quickly lots in comparable subdivisions have sold, indicating real demand velocity

- Active versus pending listings reveals current competition and market liquidity

- Individual lot modelling accounts for variation in buildability across a subdivision, since corner lots, rear lots, and irregular parcels carry different values

- Minimum appreciation threshold of 1.5x price per acre on subdivided lots versus the original parcel is a widely used benchmark for profitable subdivision deals

- Assemblage potential assesses whether adjacent parcels could be combined to unlock density or access that a single parcel cannot achieve alone

Exit flexibility is an underappreciated part of market analysis. A developer who models only one exit, typically the completed development, carries more risk than one who also prices the option to resell the raw parcel if development proves infeasible. Knowing the parcel’s value in its current state sets a floor under the investment.

What are the most common mistakes when evaluating land for development?

Most land assessment failures trace back to a small set of repeatable errors. Recognising them in advance is the most reliable way to avoid them.

- Skipping sequential due diligence. Commissioning expensive engineering studies before confirming zoning compatibility wastes money on deals that a simple bylaw check would have eliminated.

- Ignoring carrying costs. Property taxes, financing costs, and insurance accumulate during the entitlement and construction period. Omitting them from the pro forma overstates returns materially.

- Overestimating yield without technical screening. Assuming a site can accommodate a given density before checking topography, access, and servicing leads to designs that cannot be built as modelled.

- Using poor-quality comparables. Fewer than three quality comps that match buildability characteristics is insufficient to justify a price. When data is thin, risk discounts are mandatory, not optional.

- Failing to contact landowners directly. Off-market deals often offer better pricing and less competition. Developers who rely exclusively on listed inventory pay a premium for the privilege.

Feasibility studies function best when they isolate unknowns early, preventing capital from flowing into projects that will become unbuildable or unprofitable. Treating a feasibility study as a live risk management tool rather than a one-time document is the practice that distinguishes experienced developers from those who learn expensive lessons.

Pro Tip: Use staged filtering to sequence your deal evaluation. Check zoning first, then environmental risk, then geotechnical conditions. Each stage should either confirm the deal or kill it before the next round of spending begins.

Key takeaways

A sound land development assessment combines a defined buy box, nine-category due diligence, residual land value modelling, and market-validated revenue assumptions to determine whether a parcel is worth acquiring.

| Point | Details |

|---|---|

| Define your buy box first | Set parcel size, zoning, geography, price, and yield criteria before evaluating any deal. |

| Run nine due diligence categories | Title, zoning, environmental, geotechnical, utilities, engineering, construction, financial, and tax all require review. |

| Calculate residual land value | Subtract total development costs and target profit from completed value to find your maximum offer price. |

| Validate revenue with real comps | Use three or more comparable sales that match buildability traits; apply risk discounts when data is thin. |

| Treat feasibility as a risk tool | Update the feasibility model as new information arrives rather than treating it as a static document. |

TESA’s approach to land acquisition and development feasibility

Developers working in the Greater Toronto Area face some of the most complex zoning, servicing, and financing conditions in Canada. TESA provides end-to-end real estate development services that cover site identification, development feasibility analysis, capital structuring, design, and construction under one roof.

TESA’s feasibility process delivers initial insights within 24 hours, giving developers and investors a fast read on whether a site warrants deeper investigation. For those looking to participate in development without managing the full process independently, the Syndicate Build program structures collaborative investment across qualified projects. Developers who want to build foundational knowledge before committing capital can access TESA’s real estate education programs to sharpen their assessment skills. TESA’s integrated divisions, covering real estate, development, and capital, mean that every engagement is grounded in underwriting discipline from the first conversation.

FAQ

What does it mean to assess land for development?

Assessing land for development means evaluating a parcel across zoning, environmental, geotechnical, financial, and market criteria to determine whether a project is buildable and profitable before acquisition.

How long does land due diligence typically take?

The land acquisition process runs 30–90 days from identification to closing.

What is residual land value and why does it matter?

Residual land value is the completed property value minus all development costs and the developer’s target profit margin. It sets the maximum price a developer can pay for a parcel without sacrificing returns.

How many comparable sales are needed to price development land?

At least three comparable sales that match the subject parcel’s buildability characteristics, including access, utilities, and terrain, are required to support a defensible price. Fewer comps require applying a risk discount to revenue assumptions.

What is the most common mistake developers make when evaluating land?

The most common mistake is skipping or rushing due diligence steps, particularly failing to confirm zoning compatibility and environmental status before commissioning costly engineering or architectural studies.